INTERNAL ACCOUNTING ENGINEERING

Allocation of Cost of Goods Sold

14. Cost of Goods Sold.

Accounts within the Cost Of Goods Sold (COGS) Account class are used as contra-accounts. Their account names and descriptions reflect their support of Sales activities.

A COGS Main-account is often organized by geographic area. Often it is organized by groups of clients. One Main-account can have several Sub-accounts, each of which can have Sub-sub-accounts. In such a case, a Sub-account might represent a group of similar, related products, where a Sub-Sub-account might represent an individual product or service.

HOW TO ESTABLISH THE COST OF GOODS SOLD.

A Contra-Account:

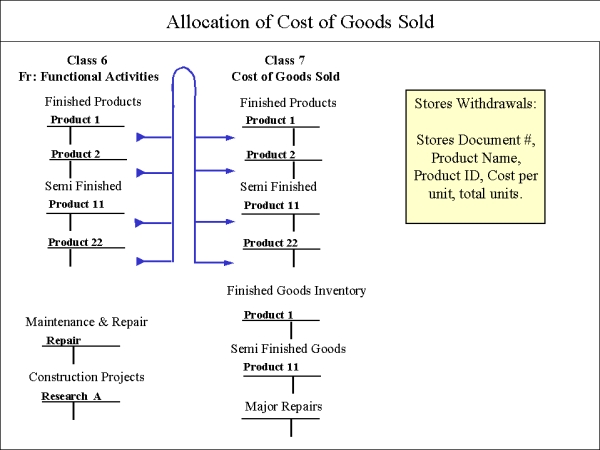

Functional Activity Production costs (Class 6) are transferred to special, Internal COGS accounts, namely, 'Finished Goods Inventory' (Class 7B). These Internal accounts are contra-accounts to specific External accounts, namely, to 'Assets, Inventory of Finished Goods' accounts. A contra-account is used to transfer amounts from Internal Accounting to External Accounting, because all External transactions must be kept separate from Internal transactions. A standard credit/debit transaction, if performed between Internal and External accounts, would result in a failed trial-balance. The contra-account of Finished Goods is used in External Accounting only at month end.

The Internal, contra-account,' COGS Finished Inventory,' does not report the difference between Finished Goods Inventory debits and Ending Inventory credits. That is left to External Accounting and its Financial Income Statement.

A Sales Transaction:

A sales transaction will withdraw finished goods from Inventory. Removing an item from stock in a sales transaction (Inventory Withdrawal Source Document) is an important Internal transaction. A sales credit to Stores Withdrawal (Class 2) will be debited to COGS (7A). The credit amount is computed as (quantity * unit production cost). Manager's can now track, at a low, inventory level, each unit (or group) sold. A computer's speed and accuracy, combined with this method, can support a true perpetual inventory control.

Special Absorption of Administrative and Sales Costs

The Manufacturing Cost of each unit sold is a combination of raw material (Class 2), direct labor (Class 4BD), and absorbed indirect costs (Class 4CD). Now we must add to this Manufacturing Cost, all Administration and Sales Department Costs (Class 4AD). Administration and Sales Department Costs should also be transferred to COGS (Class 7A). To do this, a standard absorption base is ideal, and any effort expended to design one is worthwhile. But even a simple base is sufficient in Internal Accounting to provide a reliable and practical report.