INTERNAL ACCOUNTING ENGINEERING

11. Absorption of Direct Production Departments Operating Cost

Internal Accounting dedicates specific internal accounts to apply direct and indirect costs to production, to any level of detail required, using any standard rate one devises (labor hours, machine hours, other). Internal Accounting recommends charging Raw Materials and Direct Labor costs to Production via Efficiency Variance accounts.

Internal Accounting will also support linking a machine's maintenance with specific Job-Orders, we can also use a certain base-line (i.e., machine hours) to Re-absorb maintenance to specific Job-Orders.

Accounts in Class 5 receive charges from Direct Production Department's Operating Cost accounts in Class 3 by absorption rates, and accounts in Class 6 transfer monthly finished goods to Inventory in Class 7.

The precision of this kind of Cost Accounting lets Managers track detail trans-monthly charges to jobs and products at a glance.

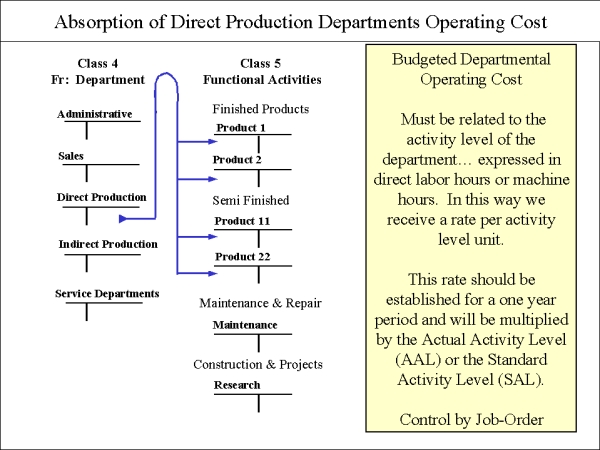

The Internal Cost Accounting structure operates like this:

Amounts were allocated (and re-allocated) to various departments, using 'To Department' accounts in Class 3.

Now these amounts will be taken

from these departments, using 'From Department' accounts (Class 4), and will be 'absorbed' by

the different Functional Activities.

Absorption proceeds by means of an annually pre-determined Absorption Rate for each product.

There are many kinds of Absorption Rates to choose from. Some use Direct Labor hours as a distribution base, others use machine

hours, others use some other base. The establishment of Direct and Indirect Production Departments Absorption Rate should be analyzed

carefully. Thanks to computers speed and precision, accountants can now give each Production Department its own unique Absorption rate, and still

manage the complexity.

To add to the accuracy of Internal Accounting, it is preferred that the individual Job-Order

should absorb the Departmental Operating amounts. The complexity of this procedure will reward the

management with unusual precision in Cost

Accounting.