INTERNAL ACCOUNTING ENGINEERING

10. Absorption of Direct Labor

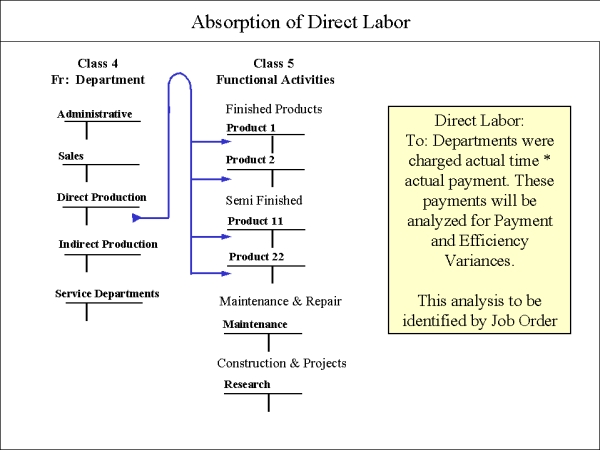

Product Cost Accounts will ABSORB Direct Labor and Departmental Operating Costs, using both Direct Labor Cost absorption, and Departmental Operating Cost Rate absorption.

Budgeted Departmental Operating cost must be related to activity level of the department; expressed in direct labor hours or machine hours. In this way we receive a rate (dollar amount) per activity level unit. This rate should be established for a one year period. Rate will be multiplied with the actual activity level (AAL), or the standard activity level (SAL),

To Departments were charged actual time worked times actual payment. These payments will be analyzed for payment and efficiency variances – This analysis should be identified by Job order.

Actual Time * Actual Payment: ( At * Ap)

Actual Time * Standard Payment: (At * Sp)

Standard Time * Standard Payment: (St * Sp)

Direct Labor Efficiency Variance:

Class 4 transfers Direct Labor transactions to Class 5 at a STANDARD RATE.

Because of this we can report the Variance between the Actual and Budgeted (Standard) amounts.

Direct Labor is usually tracked as a Variable Cost, that is, one which varies along with the rises and falls in Product output. However

Internal Accounting tracks Direct

Labor as Fixed Cost, and notes Direct Labor for its LACK of rising and falling with Product output, because wages are typically paid by the hour, regardless

of output, and not by piece-work, which alone is tied to output.

If we wish to track the Efficiency of Labor, or compare workers with their past performance or performance of their peers, we use a Labor Efficiency Variance

methodology (comparing actual labor time against budgeted time) by Product or

Job Order. It is done this way:

-

Make a Direct labor Budget. This involves setting the Rate for Labor time expended on a given product.

-

Charge a Direct Production department with Actual Direct Labor wages paid, then compare this amount with the budgeted amount.

-

To compute Labor Variances, charge a holding Department account with a Standard Labor cost.

-

Compare the Actual Cost with the Standard Cost

That's the methodology at a high level. Let's get down to more details.

HOW TO COMPUTE STANDARD LABOR COST:

1) Charge Direct Production Departments (Class 4) at Actual Cost (Ah * Ap) where Ah = Actual Hours, and Ap = Actual Price

2)

Charge Direct Labor to Production (Class 5) at Standard Cost (Sh * Sp)

where Sh = Standard Hours, and Sp = Standard Price.

HOW TO COMPUTE LABOR VARIANCE:

1. Create two new accounts for Direct Wages variances:

A. Payment Variance accounts

(4-1-95-008)

B. Efficiency Variance accounts

(4-1-96-008)

2. Compute Payment Variance = the balance of DR and CR after Direct

Production Departments (Class 4) CR (Ah * Sp) to Payments Variance, and then DR

Efficiency variance (Sh * Sp).

How An Advanced Internal Accounting Structure Develops An Absorption System.

Within the Class 5 structure, there are accounts referring to all the Functional Activities. These accounts will be debited with the absorbed values that are transferred from different department accounts in Class 4. The Direct Production Departments are the most important departments that will apply their Departmental Operating Cost to the different Production cost accounts in Class 5, by Job Order.

These Direct Production Departments work to fulfill the quantity of production planned by management. Their departmental operating cost is budgeted in order to meet production requirements established by management.

As seen in this exhibit, the first group of accounts in Class 5 will start with the Production Cost Accounts of the Finished Products. These product will finally be transferred from Class 6 to the Inventory of Finished Products in Class 7.

The next group of Class 5 accounts refers to the purported Semi-Finished Products, produced with the purpose of being used in the final production line. Normally these Semi-Finished Products will not be sold. From the Production Cost Account, these products enter the inventory of Semi-Finished Products.

This step applies to the Production cost accounts, the corresponding part of the departmental operating cost of the Direct Production Departments. The next step would be to use the same procedure with the departmental operating cost of Direct Production Department while working with the Semi-Finished Products.

As soon as the Indirect Production costs (from Class 4 ) are fully applied to the Functional Activity accounts in Class 5, the amounts charged to these activity accounts can be analyzed.

The values we charged to the Direct Production Departments in Class 3 are the amounts transferred from Class 4 to the Finished Product accounts. Remember that the Direct Production Departments in Class 3 were not only charged the Indirect Operating Cost of the department, but also reallocated amounts of different departments that gave some type of support to the Direct Production Departments.

These conditions must be realized to fulfill concept of an Activity Based Costing system (ABC).