INTERNAL ACCOUNTING ENGINEERING

8. Absorption of Indirect Departments Operating Cost

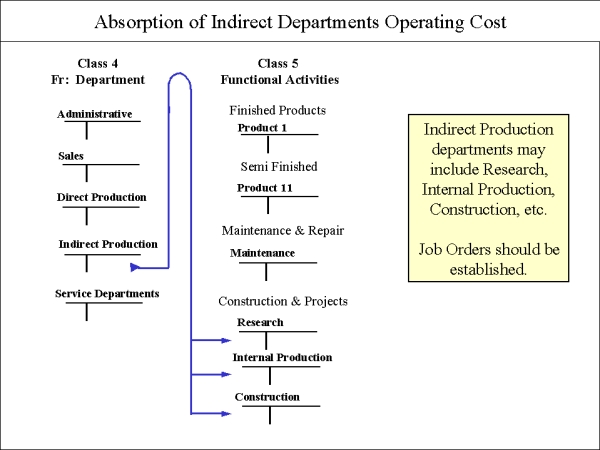

The Internal Cost Accounting structure operates like this:

Amounts were allocated (and re-allocated) to various departments, using 'To Departments' accounts. Now these amounts will be take from the departments, using 'From Departments' accounts, and will be absorbed by Functional Activities.

Absorption proceeds by means of an annually pre-determined Absorption Rate for each product.

There are many kinds of Absorption Rates to choose from. Some use direct labor hours as a distribution base, others use machine hours, others use some other base. The establishment of Direct and Indirect Production Department Absorption Rate should be analyzed carefully. Thanks to computers, accountants can now give each Production Department its own unique Absorption rate, and still manage the complexity.

As soon as the Indirect Production costs (from Class 4 ) are fully applied to the Functional Activity accounts in Class 5, the amounts charged to these activity accounts can be analyzed.

Indirect Production Departments costs absorption can be complex. Maintenance and Repair departments, in some companies, are critical and costly. In these cases, perhaps a preventive maintenance budget will help establish absorption rates. At the same time, it is not worthwhile to prepare a very complicated absorption system. A simple structure can often give adequate information. After a year or two of use, it may be appropriate to fine tune the absorption system.

The values we charged to the Direct Production Departments in Class 3 are the amounts transferred from Class 4 to the Finished Product accounts. Remember that the Direct Production Departments in Class 3 were not only charged the Indirect Operating Cost of the department, but also reallocated amounts of different departments that gave some type of support to these Direct Production Departments.

These conditions must be realized to fulfill the concept of an Activity Based Costing system (ABC).

To add to the accuracy of Internal Accounting, it is preferred that the individual Job-Order absorb departmental amounts, and not just product groups or even individual products. The complexity of this procedure will reward the accountant with unusual precision in Cost Accounting.