INTERNAL ACCOUNTING ENGINEERING

Absorption of Maintenance and Repair Departments Operating Cost

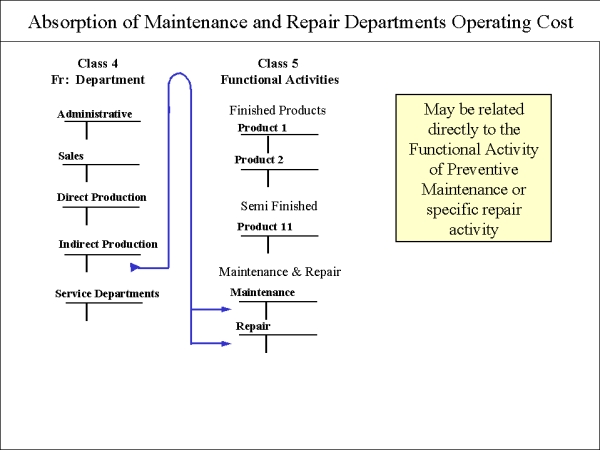

7. Maintenance and Repair Accounts

The Internal Cost Accounting structure operates like this:

Amounts were allocated (and re-allocated) to various departments, using the class identified with the 'To Departments' accounts. Now these amounts will be taken from the departments, using 'From Departments' accounts, and will be absorbed by Functional Activities.

Absorption proceeds by means of an annually pre-determined Absorption Rate for each product. There are many kinds of Absorption Rates to choose from. Some use direct labor hours as a distribution base (or cost driver), others use machine hours, others use some other base. The establishment of Direct and Indirect Production Department Absorption Rate should be analyzed carefully. Thanks to computers, accountants can now give each Production Department its own unique Absorption rate, and still manage the complexity.

As soon as the Indirect Production costs (from Class 4 ) are fully applied to the Functional Activity accounts in Class 5, the amounts charged to these activity accounts can be analyzed.

Maintenance and Repair activities are also tracked within Functional Activity accounts. An ordinary preventive maintenance budget

provides special accounts for these activities, (for example, special building maintenance, vehicle maintenance, machine maintenance, and so on).

'To' Maintenance and Repair accounts registered under Functional Activities are charged materials, labor and

absorption, and the resulting values are then transferred

either back to some Direct Production Department, or sometimes (as in the case of a specific building or machine maintenance) such amounts are

transferred to a Production management department.

However, if machine maintenance directly affects a machine used on specific Job-Orders, we need a certain base-line to charge this

maintenance to these Job-Orders. Machine hours could be used as a Re-absorption base.

Repair costs, such as a portion of operating costs of trucks and key vehicles, or key machines, should have special repair accounts with

detailed information about the spare parts cost, labor cost, and absorbed amounts. These repair costs

could be re-absorbed by Job-Orders linked to these machines, or to departments which used the vehicles.

Departmental operating cost of Maintenance and Repair may be related directly to the functional activity of preventive maintenance or specific repair activity. This absorption must be based upon specific information by the maintenance and repair departments. Control should be realized by job order system. A global amount would be absorbed.

Under Indirect production departments there may be departments related to Research, Internal production construction, etc. Job orders should be established. General information will be sufficient.

How an advanced Internal Accounting Structure Develops a Cost Absorption System.

Within the Class 5 structure, there are accounts referring to all Functional Activities. These accounts will be debited with the absorbed values that are transferred from different department accounts in Class 4.

As seen in the previous exhibit, the first group of accounts in Class 5 will start with the Production Cost Accounts of the Finished Products. These products will finally be transferred to the Inventory of Finished Products.

The Maintenance and Repair Departments operating cost will be taken to the specific Repair Cost accounts in Class 5, Group 4. Finally, charge the Construction Cost account with the amounts of Indirect Cost for departments who worked with these construction projects.

As soon as the Indirect Production costs (from Class 4 ) are fully applied to the Functional Activity accounts in Class 5, the amounts charged to these activity accounts can be analyzed.

Under special circumstances some of the Maintenance Costs can be reapplied to the Finished Products Production cost accounts. An example: if equipment is used consistently during a fiscal year with the same final product; the monthly Maintenance Costs of this equipment could be reapplied to the Finished Product account.

Both the Repair Cost and the Cost of Constructions projects should be taken monthly to Class 7, which should have accounts for keeping these investments with the assts.