INTERNAL ACCOUNTING ENGINEERING

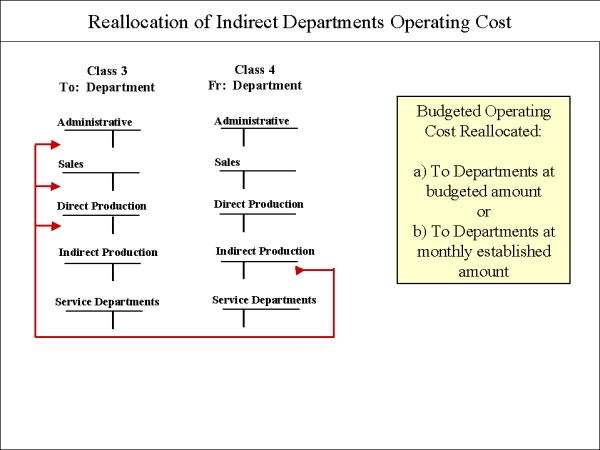

Reallocation of Indirect Departments Operating Cost

5. Indirect Production Departments

Indirect Production Departments work indirectly with production. They include maintenance, repair, quality control, configuration control, and research and development departments. Sometimes much analysis is needed to determine the exact placement of a department.

Budget operating cost reallocated:

|

To other departments at budgeted amount | |

|

To other specified departments at monthly established amount |

|

Maintenance and repair costs could be absorbed by functional activity |

Reallocation Procedure

We must reallocate the operating costs of the Indirect and Service departments not only to the Direct Production departments but also to all other departments in our company that are receiving these different services. The Maintenance and Repair work may also have been realized in some Administrative or Sales department. So the whole question of reallocation is a serious and important procedure.

The responsible person for each department of the company will have to prepare their specific operating cost budget for the fiscal year and calculate the monthly average amount.

Budgeted Procedure

Once we have established the average monthly operating cost of the different Indirect and Service departments, we must calculate how much of these operating costs will be charged to the different receiving departments. This established dollar amount will be the reallocated value that we will transfer each month to the receiving departments.

This monthly amount will be used during the whole fiscal year, however, if special new conditions arise, we may change these monthly amounts. At the end of each year we should verify if these budgeted amounts are still acceptable or should be changed. We should not reallocate monthly the actual operating cost, but the pre-established budgeted amount.