INTERNAL ACCOUNTING ENGINEERING

Reallocation of Service Departments Operating Cost

4. Service Departments

Service Departments include janitorial, medical, security departments, cafeteria and so on. These departments are special because we Re-allocate the amounts charged to it to other departments which received its service.

Quality control departments may be treated as Service Departments, and their amounts re-allocated. But an R&D departments costs should be applied to specific product projects. Project Accounts can be treated as production Job-Order accounts. Variances between actual departmental operating costs and absorbed amounts are discussed in another section of this web site.

Cost Re-Allocation Procedure

Service Department operating costs must also be allocated. Lets take the example of a Maintenance department:

The budgeted operating cost of a Maintenance department was set at $10K per month, including salaries, wages, rent, depreciation, insurance, office-supplies and so on. The actual departmental operating costs were allocated to this department. However, these costs will NOT be absorbed by

production. There is no clear relationship between Maintenance departmental costs and production activity.

Instead, since this Maintenance department served other departments with its activity, we will Re-allocate these operating costs to

departments served.

This is the procedure of Re-allocation: When we prepare the budget of the Service Departments, we

also identify the Re-allocation base.

While it is complicated, again, too much detail on this step is not worthwhile. Our matching of Re-allocations must be simple and

clear. We may simply decide on a set monthly base to be Re-allocated to the other (Admin, Sales, Direct and Indirect)

departments served. Such bases are subject to annual revision.

Re-allocated amounts will be credited to departmental accounts specifically for that purpose, which accept only re-allocated

values. Actual departmental operating costs will be debited to a separate departmental account.

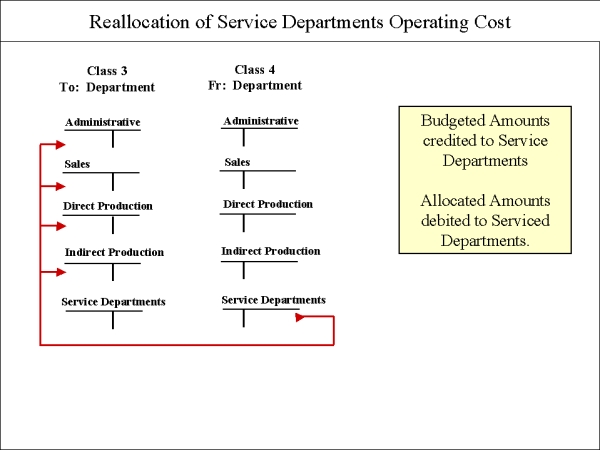

The preceding exhibit displays the procedure. We have opened two classes of accounts: one class to charge the operating costs TO the Service

departments, and one to transfer these operating costs FROM the Service departments to other departments.