INTERNAL ACCOUNTING ENGINEERING

Allocation of Direct Material

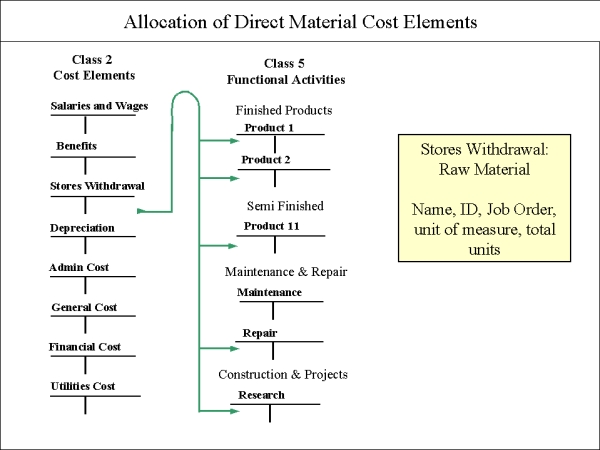

3. Direct Material Transactions.

Direct Material costs are allocated to Product Cost accounts, not to Departments.

A key factor in Variance Reporting is Stores Inventory data. There are three

kinds of Stores Withdrawals: Supplies withdrawals for Departments, Raw Materials withdrawals for Production, and Inventory withdrawals for Sales.

![]()

Allocation of Direct Material Procedure:

Stores Withdrawals for Direct Material (2-3-00) are charged to Production (5-n). Internal Accounting uses a Standard Cost basis in the following manner: Actual prices and quantities are transformed using Internal accounts into a Price Variance with the formula, ((Aq*Ap) - (Aq*Sp)), and then into an Efficiency Variance with the formula ((Aq*Sp) - (Sq*Sp)). Finally, the amount (Sq*Sp) is charged to the Product Job Order.

Direct Materials Efficiency Variance:

Materials Efficiency Variances will report the actual count of materials withdrawn for the

job order,

compared with a Budget.

Efficiency Variances (for expired portion of expenditure only) compare Standard (budgeted) Usage vs. real materials Usage. The stores withdrawal algorithm is:

Efficiency Variance (Aq*Sp) - (Sq*Sp)

where Aq is Actual Quantity, Sq is Standard Quantity, and Sp is Standard Price.

Direct materials Price Variance:

For Price Variance reports we focus upon Raw Materials withdrawals. If we

withdraw something from Stores this month, there is no guarantee it will have

the same Actual cost as last month. It may vary from our Budgeted, Standard

costs. The monthly variance can be measured by reporting Stores data.

1. PURCHASE PRICE VARIANCE: Purchase Price Variances will report the

actual cost of materials withdrawn for the job order compared with a Budget.

Price Variances (for expired portion of expenditure only) compare

Standard (budgeted) prices vs. Vendor Invoice prices. The stores

withdrawal algorithm is:

Price Variance 2-3-01-005 (AQ*AP) - (AQ*SP) where AQ is Actual Quantity, AP is Actual Price, and SP is Standard Price.