INTERNAL ACCOUNTING ENGINEERING

Allocation of Direct Labor

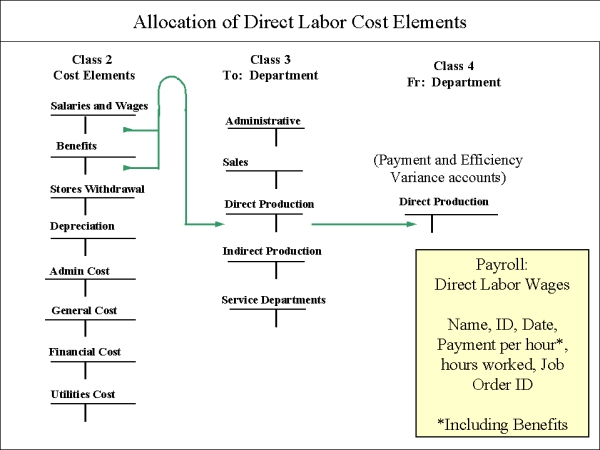

2. DIRECT LABOR TRANSACTIONS

Basically, Class 2 mirrors Direct Labor wages recorded in Class 1. (A minor exception is when a calendar period disagrees with another definition of month-end, since there will be a days overlap on a calendar. This must be noted.) Class 2 recognizes the total payment as Direct Labor. Class 3 then awaits a detailed allocation of Direct Labor wages to the various departments. The External procedure to record Direct Labor payroll is:

Credit: Accounts Payable -- Payroll (Class 0) Debit :

Expenditure -- Direct Labor wages (Class 1).

In A/P one general account suffices for both salaries and wages. But to support Internal Accounting, an Expenditure Main-Account should be developed especially for Direct Labor wages. By structuring Payroll by departments, we isolate Direct Labor wages from other payroll and provide a more accurate cost accounting.

The Internal procedure to record Direct Labor payroll is.

Credit : Cost Elements -- Direct Labor wages (Class 2).

Debit : Direct Production Department (Class 3).

Direct Cost Allocation Procedure

Direct labor wages are normally Variable costs, charged directly to the Production Cost Account, what is commonly called

WIP. It is commonly held that direct labor wages change proportionally to the

changes of the production level.

In fact, however, hourly wages are only related to a time unit, not to pieces produced. True direct wages are piece-work wages,

but very few industries pay their workers by unit of production. We should have the option to treat a direct labor wage as

a fixed cost, just as salary is a fixed cost. Monthly or hourly, these payment are paid by time interval, not by production

unit!

In any case, we should always allocate direct labor wages to the corresponding Direct Production department. The amount to be

allocated to such departments will correspond to the total earned direct labor hours for the period, the actual cost of direct labor

recognized for this Direct Production department.

Job-Orders absorb these actual direct labor wages. The amount will vary proportionately with the activity level of production. The

absorbed direct labor wage, we can agree, is the correct 'variable' cost of direct production (not to be confused with 'variances').

Actual costs charged to Direct Departments will be compared with budgeted amounts at month end, to report Variances for managers.

Internal Accounting automatically allocates direct labor costs to direct

Production departments, and re-allocates indirect labor costs to direct

Production departments, and provides the option to treat direct wages

as fixed rather than variable to production (based on the premise that piece wages are the only

true variable wages). When products absorb costs of direct labor hours this way,

Internal Accounting can report absorbed direct labor cost as a standard cost.

Internal Accounting variance reporting is more accurate and meaningful in reporting

variable costs of direct production.

Internal Accounting provides Labor Payment and Efficiency Variance accounts to track variations in direct labor to product output, and ease the

shock of sharp rises or declines in internal activities, and also allows managers to track Variances in labor costs.

Here's how it works: Payroll transactions (2-1) are charged at (Ah * Ap) to a Payment Variance (2-1-98), then computed using the

formula, ((Ah * Ap) - (Ah * Sp)), and then an Efficiency Variance is

computed with the formula ((Ah * Sp) - (Sh * Sp)). The difference between the two figures in each formula is the variance.

Finally, the amount (Sh * Sp) is charged to the Product Job Order.