INTERNAL ACCOUNTING ENGINEERING

Allocation of Indirect Cost.

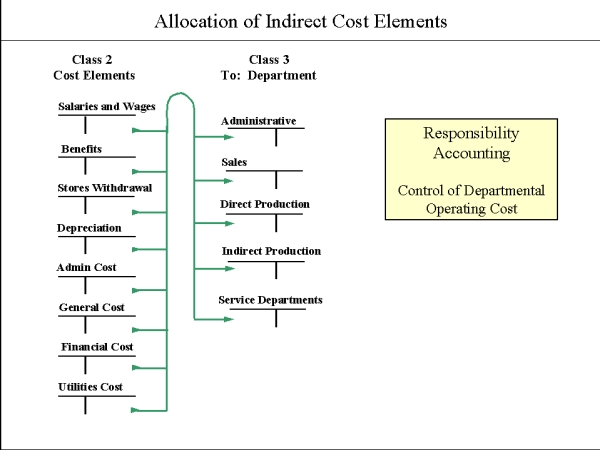

1. Indirect Cost transactions.

In Class 2, the Cost Elements class, we have recorded all costs which match this accounting period and correspond to its production volume. All cost elements within Internal Accounting must be allocated. The first step in this procedure is to allocate all Indirect Costs to the various departments.

Indirect Costs

We begin by allocating all of our indirect costs to the different departments (or cost centers). All costs that are not classified as direct, and that have their origin in our departments, will be indirect.

To give our direct laborer an opportunity to produce a product, we must establish a department with all the necessary costs it will require to operate this department. So we must have in this department an employee who is paid a salary and who will be responsible for the activity within this area. We will also need an indirect laborer who will oversee the operating procedure of this department. Naturally, we also need a space (rent), electricity, insurance, phone and many other indirect costs in order to obtain the smooth operation of this department.

All of these indirect costs must be allocated to some specific department or cost center that we have established in our company. This means that we are not only interested in controlling the operating costs of our production departments, but also the operating costs of all other departments that we have in our company.

Under the Responsibility Accounting system, we have to control our:

|

Administrative and Sales Departments | |

|

Direct and Indirect Production Departments | |

|

Service Departments. |

Following is the basic departments code structure of our Internal Chart of Accounts:

|

3-1-00-000 |

Administrative and Sales Departments |

Each of these departments will be charged with their specific operating costs. |

|

3-1-01-000 |

Administrative Departments |

|

|

3-1-01-001 |

President's Office |

|

|

3-1-05-000 |

Sales Departments |

|

|

3-1-05-001 |

Sales Manager's Office |

| 3-2-00-000 |

Direct Production Departments |

This operating cost is matched to the activity of the fiscal period. |

|

3-2-01-000 |

Specific Department A |

|

|

3-2-05-000 |

Specific Department B |

| 3-3-00-000 |

Indirect Production departments |

One person in each department is responsible for preparing his/her specific departmental operating budget. |

|

3-3-01-000 |

Quality Control department |

|

|

3-3-11-000 |

Maintenance departments |

|

|

3-3-21-000 |

Repair departments |

|

|

3-3-51-000 |

Research and Development |

| 3-4-00-000 |

Service Department |

|

|

3-4-01-000 |

Janitorial Department |

|

|

3-4-03-000 |

Security Department |

|

|

3-4-07-000 |

Cafeteria |

|

|

3-4-11-000 |

Inventory Department |

|

|

3-4-15-000 |

Fitness Department |

Indirect Cost Allocation Procedure

Indirect Costs are normally

identified as Fixed Costs, and their allocation is usually simple: salaries and wages are charged to managers and

other personnel who are not directly engaged in production; rent is

prorated to departments; office supplies are charged to each department; depreciation is charged to machines and other fixed

assets within the department, and so on.

However, some indirect costs are not so simple to allocate to a specific department, for example, a telephone bill for the whole

company. It is not worthwhile to analyze each phone call. In this

case, we have a choice:

1. Allocate the total phone bill to only one department, such as the General Managers, or

2. Allocate a pre-established percentage of the bill to several departments. This method may have to be revised annually to

reflect changing conditions.

It is possible to spend more time on these indirect cost allocation exceptions than is worthwhile. Indirect cost allocation should be

kept simple but effective, giving management an accurate, reliable

operating cost picture of all departments, without petty details.

Most Fixed costs are Indirect costs. Similarly, most Variable costs, for example raw materials, are Direct costs, and should be

allocated to the Production Cost account.

An Exception of Direct Cost:

Department Z assembles refrigerators. Each refrigerator requires 16 screws and 4 bolts, but Department Z receives these parts in full cases. The cost of a case is charged to

the department, and later this cost will be absorbed as part of the

indirect cost by multiple job-orders during the period.

Actual costs allocated to specific departments in this way can be compared with budgeted amounts very simply. A budget is not part

of GAAP, but is management data prepared outside of an accounting system. The Internal Accounting structure, however, harmonizes perfectly with, and may be directly compared to, budgeted

departmental operating costs.

This clarity gained in comparing actual to budgeted amounts, along with the Variance reports resulting from the comparison, is a major

step forward in gaining relevance in Cost Accounting.