As previously indicated, the Job Order system and the Budgets for the Production, must express their amounts in Standard Cost. We just cannot plan, cannot prepare Budgets, without having created Standard cost. It is not acceptable, when we are informed that we do not need to have established standard values.

We should not include in the Production Cost actual amounts. Such procedures would create monthly variances in unit cost - and accounting would not be able to explain these monthly variances. We have to separate the different variance on specific accounts. These accounts would identify such variance as purchase price and efficiency variance. We must also separate these variances for Direct Material and Direct Labor.

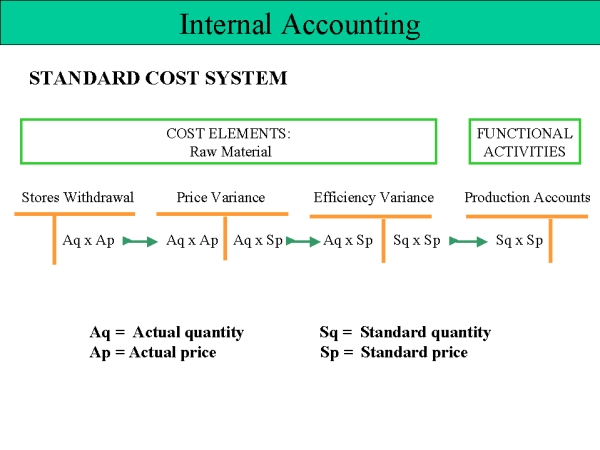

We recommend to use following specific accounts, which would make it easier to understand the origin of these variances. Let us study the following Exhibit 31:

Exhibit 31

This presentation is a very basic and well known structure. We suggest that our purchase of Raw Material will be recorded in the Material Inventory account of our Assets, at the actual quantity times actual price.

From the Direct Material inventory we withdraw the actual quantity that we need for our production and at the actual price. This actual price may be calculated in different ways, but it just will be some value we may identify as "actual".

From the Stores Withdrawal - we will transfer this amount to the Price Variance account. We will now compare the value of Actual Quantity times Actual Price, with the amount we may obtain when we multiply the Actual Quantity time Standard Price. This difference between debit and credit amount will be the Price Variance referring to the amount use in the production of this Job Order.

From Credit of this Price Variance account we till transfer this amount to the debit of the Efficiency Variance account. Here we will compare the Actual Quantity with the Standard Quantity. So here we have the Efficiency Variance.

This amount of Standard Quantity multiplied with Standard Price will be transferred to the Production Cost account. This is a very simple presentation, but very important to realize so we will receive a production at Standard Cost.

The same basic procedure would be followed to control the actual values for Direct Labor with standard values. Let us analyze the next two Exhibits.

Exhibit 32

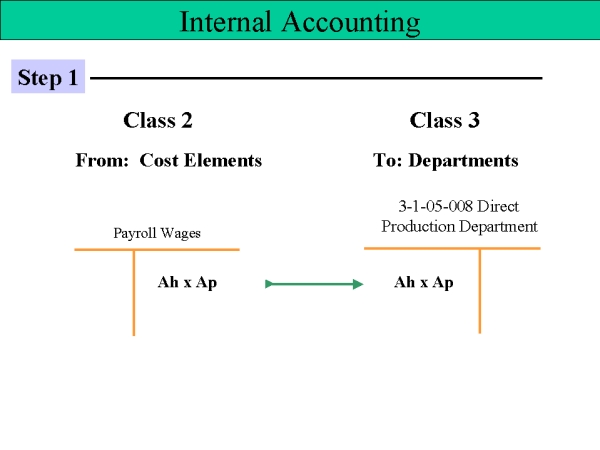

Here naturally we do not have some account that would correspond to the Inventory withdrawal. We use the Payroll from External Accounting with all necessary details. We know the ID of the Direct Labor worker, the department to which this worker is assigned, the payment per hour, the Job Order with which he worked and the time he spent with this Job Order.

These are the basic details that the Internal Accounting requires to establish the Direct Labor cost for a specific Job Order. In Class 2, Cost Elements, we will credit this amount on our Payroll Wage account. This same amount will be taken to the Direct Production Department, where the Worker is assigned. This amount is the actual cost of Direct Labor corresponding to this Direct Production Department.

This next Exhibit [ Step 2 ] will show us the specific accounts that we need to identify the Payment and the Efficiency Variance. All these accounts are recorded within Class 4 : From Departments.

Exhibit 33

The Payment Variance account will compare the actual value of this Direct Labor cost with this Direct Labor expressed in Standard Payment. We receive here the amount of the Payment Variance. The next account in this Class 4, will be used to identify the variance related to the Direct Labor Efficiency. This amount will now be applied to the corresponding Production Cost account in Class 5. We control this production with a Job Order procedure.

Let us here remind you again, that we recommend to use of Standard Cost when referring to Direct Material and Direct Labor. The Standard Costs are the building blocks of our Production Budget.

When we refer to the Departmental Operating cost [the Indirect Cost], we should use the budgeted values.