![]()

![]()

![]()

![]()

![]()

![]()

|

|

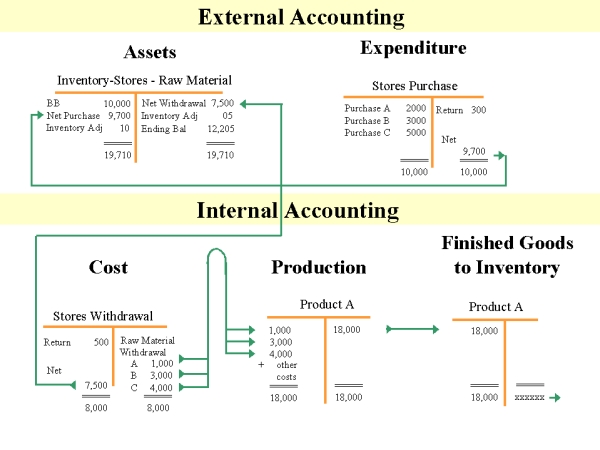

INTERNAL ACCOUNTING ENGINEERINGDIRECT MATERIAL INVENTORY TRANSACTIONS.Let us now discuss how the accounting transactions that are related to Direct Material, will be recorded in this new External and Internal structure. Today in the External (Financial) Accounting we do not have any Expenditure account that will show management how much Direct Material we have purchased during this month (accounting period). The purchased amount will be debited directly to the Direct Material Inventory account. If we develop an External and Internal Accounting structure, we will be able to create special Expenditure accounts that will report to management how much Direct Material we have purchased this month. In the following Exhibit we will analyze this new procedure step by step.

Exhibit 18: In the upper part of this exhibit we are showing the transactions realized in the External Accounting. Every time we purchase some Direct Material (or any other Inventory item) we should debit this amount in the corresponding Expenditure account. Here we can see that during this month (accounting period) our company realized three different purchases. The total amount of these purchases we record in the debit of this account. In this example we credit this Stores Purchase account with our return of 300 Dollars. At the end of this month, we have a debit balance, which we will credit the Stores Purchase account and transfer to the debit of the Inventory Stores - Raw Material. In this Asset account we have a beginning balance - to which we add the net purchase. The Stores Withdrawal ( Raw Material, Supplies, Parts) correspond to Internal Accounting. We have created this account under the denomination of Cost Elements. All Raw Material withdrawal must be credited this account - and debited directly to the Production Cost Account. Here it is indicated, that the stores withdrawal correspond to the Product A. And there have been 3 different withdrawals ( A, B and C). To the debit of this Stores Withdrawal, we have to record the return of some material. The credit of this return will be recorded in the Production Cost account of Product A. In this exhibit the credit of this return is not shown. During the month-end closing procedure, the net amount of the Stores Withdrawal will be transferred from debit of this account to the credit of the Asset account: Inventory Stores Raw Material. In this account, are also recorded any type of inventory adjustments. As we can observe, the new procedure provides much more clarity than what can be obtained using only Financial Accounting. The benefits of separating Financial from Internal Accounting are immense.

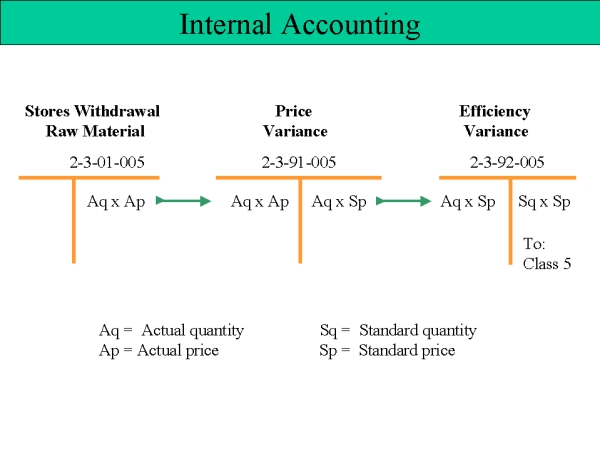

RAW MATERIAL STANDARD COSTINGOn the subject of raw material that is withdraw from Stores Inventory to use for production - let us here clarify how we could express this withdrawal in some Standard Cost measurement. Exhibit 19 shows this type of procedure.

Exhibit 19 - The Stores Withdrawal - Raw Material will be credited with the actual amount that we are taking out of this store and expressed with the actual price. This amount will be taken to the Price Variance account - and we will compare this amount with the value of the actual Raw Material used at the Standard Price that we have established in advance. The variance between the debit and credit amount on this account, will refer to the Price Variance of Raw Material used in production. The credit amount from this account, we transfer to the debit of the next variance account: the Efficiency Variance. The credit amount on this account will be representing the Standard quantity that we should have used for this production, multiplied with the Standard Price per unit of Raw Material. Finally, this amount ( Sq x Sp ) will be charged to the Production Cost account of this product realized and controlled by a Job Order system. |