![]()

In the Fundamental Overview and section on Structure and Development, we have studied the basic idea of the importance of

having the Internal Accounting structure separate from the External-Financial Accounting.

Let us now study how this new structure would developed.

This next Exhibit is of an INTEGRATED ACCOUNTING system. The Integration correspond to the application of having both External and Internal accounting under a single Chart of Accounts structure.

.

Exhibit 23

Previous exhibits have given us the important concept of how we should separate the External -Financial Accounting from the Internal. Exhibit 23 is the total structure, which integrates both the External and Internal accounts.

Our primary focus in this Website - is the Internal Accounting structure. The internal portion that starts with the column identified with the name Class 2 and finishes with Class 7.

This internal portion of the total integrated structure is the necessary Chart of Accounts specifically designed for Managerial information needs.

The Internal portion of our Chart of Accounts:

.

Exhibit 24

![]()

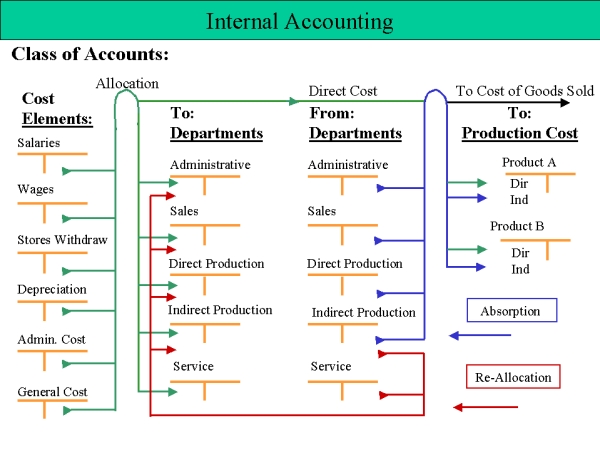

Cost Allocation:

All Cost Elements ( Class 2) that correspond to this time period and to the Functional Activities and Sales, are registered under this Class 2.

Because in the External Accounting we have debited our Expense Accounts with the amounts that correspond to the period, consequently we will have to start our Internal Accounting by crediting these Cost Element accounts. The total amount that are posted to these Cost Element accounts, correspond basically to the same amounts that we have debited to the Expense accounts.

The principal difference between Expense and Cost values is the basic point of Matching the Expense toward the Revenues and in the Internal Accounting this Matching principals is also referring to the Production Cost account ( the account that we today call Work in Process Inventory, which is a totally wrong identification of this account).

These total Cost Elements in Class 2 - correspond, as you will understand, to the amount with which the Internal Accounting starts with.

From Credit of class 2 - we ALLOCATE these cost to the different accounts where they correspond.

We will divide these Cost into following basic three groups:

1) Indirect Cost - they will be allocated to the different departments that we have established in Class 3.

2) Direct Cost - they will be allocated to the different Functional Cost accounts that we have established in Class 5.

3) Cost of Goods Sold - they will be allocated to the different Cost of Goods Sold accounts that we have established in Class 7.

Exhibit 25

So the total amount in Class 2 - Cost Elements - is allocated to the following Classes: 3- Departments, 5- Functional Activities and 7 - Cost of Goods Sold.

By allocating the Indirect Cost to the different Departments, we are following the important procedures of the Responsibility Accounting System.

Each and every department - Administrative, Sales, Direct Production, Indirect Production and Service Departments - is required to identify its Departmental Operating Costs.

We will no longer use the terminology of Overhead - it is absolutely inadequate to use such a general term, when we intend to express the operating costs of our different departments.

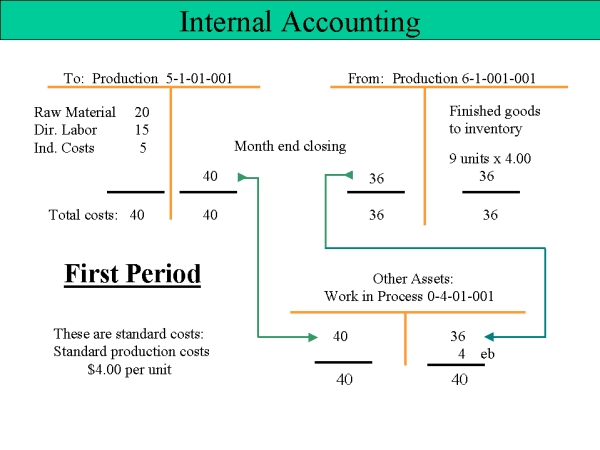

The Direct Cost , identified as direct material, will be allocated directly to the Production Cost account.

Here again we should no longer use the terminology of Work in Process Inventory, as this account is not created to show management the amount of work in process, but to tell management the production cost for this time period (a month) or for a Job order.

We strongly recommend to use a Job Order system - if the company is producing different products. But we agree also, that a Job Order system is more complicated to structure than some less specific control system.

Let us now clarify, that Direct Material is sometimes also used for repair of some machine or for some specific preventive maintenance, also when the company is producing its own machines, dies or molds. This internal production will use some direct material and also labor directly related to this job order.

The last group of the Cost Elements that we have identified, is referring to the cost of goods sold. From the Finished Goods Inventory we transfer the amount of goods sold to the corresponding account in Class 7. These cost are the production cost of our units produced and sold.

Later we will discuss the need to add to these cost of goods sold some value of our Administrative and Sales departments operating costs. With this procedure, we will fulfill the correct identification of what are our total and actual cost of goods sold.

During the accounting period we will identify all amounts debited to the Expense accounts in the External Accounting, and transfer to the Internal Accounting only the amounts that correspond to this period. To end of the month, we will have allocated all Indirect Cost to the different Departments in Class 3 of our Internal Accounting chart of accounts.

Now we will be ready to take next step referring to the Departmental Operating cost.

Re-Allocation of operating cost

We know that Direct Production Departments have specific departmental operating costs.

These operating costs are necessary for the Direct Production Departments, so they will be in position to fulfill their work orders.

As Direct Production department's must have their specific departmental operating cost to fulfill the planned production activity, all other departments in our company need their specific departmental operating cost as well. This is a logical consequence.

So Indirect Production Departments - such as Maintenance and Repair - have departmental operating cost just for the purpose to give necessary service to other departments within their activity frame.

Maintenance will give their service to both Administrative, Sales and Direct Production departments. For some Direct Production Departments a special preventive maintenance should be provided.

The same observations should be used also for the Repair departments. Their departmental operating cost is necessary to give other departments their repair service.

We may also use the same projections when we analyze the departmental operating cost of the different Service Departments. Here we would have such departments as Security, Janitorial, Cafeteria etc.

These service departments are giving their attention to many other departments of the company.

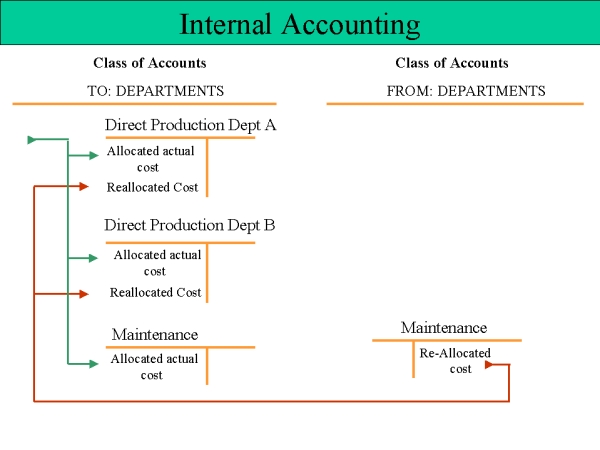

This whole presentation that we have now discussed, is telling us about the important concept of RE-ALLOCATION.

Here follows an Exhibit that tells you in a graphic form this type of re-allocation. It is a basic - simple presentation.

Exhibit 26

We have to find the right re-allocation procedure for each of the departments that we have mentioned.

The Maintenance department must re-allocate their departmental operating cost to the different Direct Production Departments, to some Administrative and Sales departments and also to some specific Functional activity accounts in Class 5 where the Internal Accounting has created accounts for the control of the preventive maintenance cost.

The Repair department must re-allocate their departmental operating cost to the different Direct Production Departments and also to some Administrative and Sales department. The repair activity of this department is not only referring to repair machines but also repair buildings and other existing structures.

In Class 5 the Internal Accounting structure has specific accounts to control more expensive repair of machines, trucks and buildings.

The different Service departments will re-allocate their operating cost in accordance to the best distribution method.

With this re-allocation procedure, we will obtain the most adequate configuration of the total departmental operating cost of the Direct Production Departments.

This is a very important course of action for our Internal Accounting development.

We will accumulate in the Direct Production Department not only the operating cost of this department, but will also add the necessary operating cost of the different departments that are giving service to this Direct Production Department.

This procedure will identify the Absorption Rate in the most accurate way. That means, that the production will not only absorb the operating cost of the Direct Production Department but also the cost of the different department that has given their service to the Direct Production Departments.

![]()

ABSORPTION COSTING SYSTEM

The next step that we will analyze with you, our Reader, is refers to the delicate question of how the production should ABSORB the departmental operating cost of the different Direct Production Departments.

This procedure may also expressed in following way:

How will we accountants, APPLY the departmental operating cost to the different products.

Let us analyze again this following Exhibit - to review the basic configuration of the Chart of Accounts for the Internal Accounting development.

Exhibit 27:

Here some explanations:

From Class: Cost Elements - we take the indirect Cost to the different departments in Class 3, and then have to realize the Re-Allocation. Now we are talking of Absorption.

The Absorption Cost analysis is referring only to the Direct Production departments.

The different products in Class 5: To: Production Cost, will absorb the Departmental Operating Cost of the Direct Production Departments in accordance with a measurement of a cost driver that we have to establish for this type of production.

We may use as this Cost Driver the measure expressed in Direct Labor hours or Machine hours.

When this method tells us that Product A used more of the Direct Labor hours than Product B, the production of Product A will have to absorb more Departmental Operating Cost than the production of Product B.

For such Absorption Cost system, we will need to prepare some pre-established Rate per a unit of the cost driver. In other words: so many Dollars of the Departmental Operating Cost per each hour of Direct Labor.

![]()

Functional Activity Accounts

Under this description in Class 5 - we open accounts related to the different products that we produce and also open accounts for Preventive Maintenance control and Repairs. Finally we also need accounts that will identify the production cost of some products that we need for our own production activity. We refer to dies, tools or machines we produce in our own company.

The traditional accounts used to identify the production cost, are the one we have learn in our schools:

These account require a name and code of the product. We will debit this account with the Raw Material, Direct Labor and the Departmental Operating cost.

Let us analyze the following two Exhibits, 28 and 29:

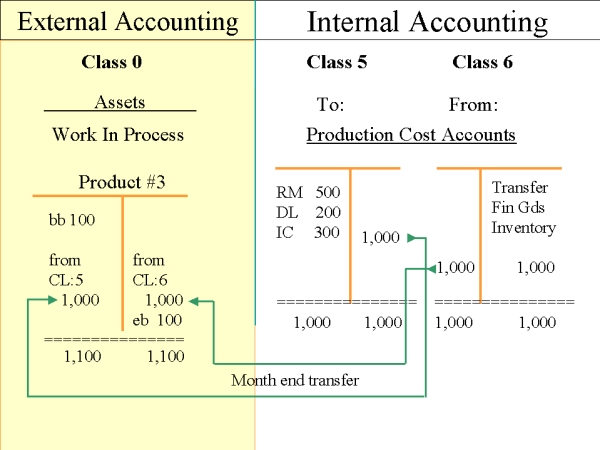

Besides Class 5: To Production, we see here also the next Class 6: From Production.

This is a classic presentation of what really is the value of Work in Process.

Analyzing this presentation, you will agree, that it is absolutely wrong to call the production cost account: W I P.

The ending balance values of Class 5 and Class 6 are transferred to Class 0: Assets - and this account we may identify as Work in Process. This account is showing management how much value is in process. This account may give management valuable information - if the value of work in process every month is increasing. This could mean, that some procedure in the production is not working correctly.

But this type of control of work in process - will only be used in Process Costing - not in Job Order Costing.

Let us just remind you:

Process Costing is used when we have a production that will be started in January and finished to end of the calendar year. For example: we produce Soya been oil; we produce cane sugar; we produce only pencil # 2.

This production during a year, may be controlled with monthly checking values and we will have some ending balance as work in process.

If we work with different products during different time periods, we should use Job-Order system. And this Job-Order will be NOT controlled by calendar month, but by starting date and finishing date. This could be a production of 10 days during the same calendar month or starting one month and ending next month. We are not interested to know how much of this Job Order was in process to end of a calendar month.

The next Exhibit is showing the procedure inside the Internal Accounting structure.

Exhibit 30

We see here Class 5 and Class 6 accounts and Class 0 Asset account, just for the information of how much of the Process- Costing was still in the department. This ending balance should be more or less the same month after month, using the process costing system. If this ending balance starts to increase, that means that something is wrong.

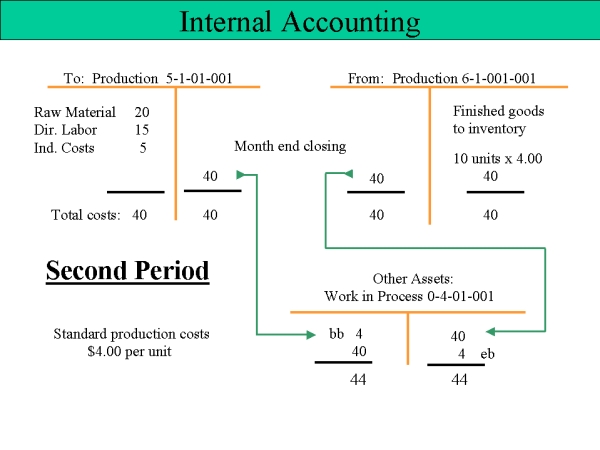

From Class 6 we will transfer the units produced to the corresponding account of Inventory Finished Goods of Class 7. In this case, we would recommend to use Standard Cost for our production, independent if the production is controlled by Process Costing or Job Order Costing.

In this Class 5 and 6 - we also have accounts to control the repair cost . We open a chart of accounts code that will correspond to repair of some specific machine. To end of each accounting period ( month ), we may transfer the accumulated value of the repair realized during this month and recorded in the debit of Class 5, of this account and we credit this same amount in Class 6 and debit it in Class 7, to a group that correspond to such type of repair. By month-end closing, we will have to credit Class 7 and debit this amount in an Other Assets account where we will keep it unto the period that this repair was finished. From this Other Asset account, we may then transfer this value of this repair of the machine to some corresponding Asset account.