An Analysis Made for the Internal Accounting Structure

By: Emanuel Schwarz

(May 1, 2000) - Previous articles featured on Pro2Net have emphasized the importance of separating the financial accounting

structure (the external chart of accounts), from the internal accounting

structure. This new Internal structure will be developed in accordance to managerial information needs.

![]()

A basic structure is necessary to arrive at an internal system that

will be perfect for cost accounting purposes. Here we will discuss the basic classes of accounts that are necessary in internal

accounting:

Cost Elements

Just as in general accounting, all expense accounts must be analyzed and matched to the sales-revenue accounts.

The same basic procedure must be realized in the creation of an internal accounting structure. However, cost is not matched to the

amount of sales, but to the production activity volume of the company.

It is important to recognize that within a company's internal accounting system, we are not interested in the amount of the sales

and revenues. The sales accounts correspond to general accounting (external accounting) and not to internal accounting.

In same way accountants are very accustomed to express themselves saying: "This cost corresponds to the inventory

account..." or "These costs will be recorded in the income statement..." We should turn away from such statements when we

dedicate our attention to internal accounting. It is necessary to understand and to remember, that internal accounting has to focus

on transactions related to the internal value movements.

Internal accounting will show how much it cost to produce a product. At

this established production cost, transfer the units produced to the finish goods inventory account in

external accounting. The next step will refer to sales activity and we will use the production cost to evaluate our

cost of goods sold.

Within this class of accounts of cost elements, all costs for this accounting period will be registered. A

very important analysis is now given to us. Establish all costs into two

basic groups:

Group 1 - All cost elements that are identified as directly related to

production will be allocated from this cost element class directly to the production class of accounts.

These direct costs are also identified as variable costs because these costs vary proportionately

with the changes in the activity level.

Group 2 - All cost elements that cannot be identified as directly related

to production will be allocated from this cost element class directly to the cost center class of

accounts. These indirect costs are also identified as fixed costs because these costs do not vary

proportionately with the changes in the activity level.

These two groups help us to allocate all cost elements to the right accounts. We identify these costs with

their association to the final cost objective of production. This is very

helpful to fulfill the next two important steps of configuring an internal accounting structure. There must be a

clear identification and structure of a responsibility accounting system and production cost accounts.

The responsibility accounting system refers to all departments and cost

centers in a company. We strongly recommend avoiding the term "overhead" (or underfoot). Use instead a more

.satisfactory word for these costs accumulated in the different departments. From now on identify these

costs as departmental operating cost.

This responsibility accounting system refers to all departments in a company and not only to the different

production departments. The universities teach that there is only one overhead account and refer only to

production departments. This is not correct. All departments in a company must be included in a

responsibility accounting system.

Let me repeat: We allocate all indirect cost to the different departments. Within each department may be

one or several cost centers. (This refers to each machine, which we like to identify as a cost center.)

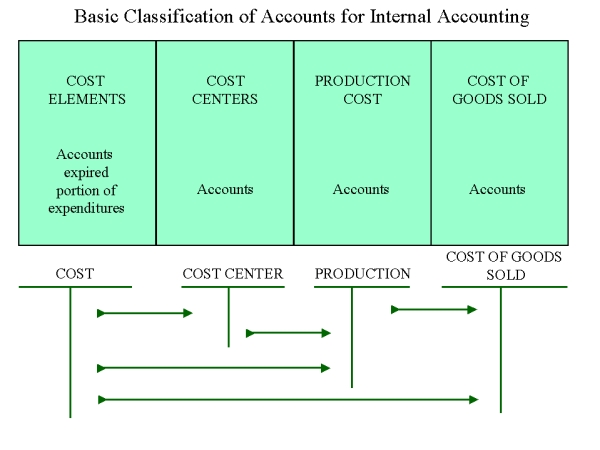

The graphic depicts to the basic structure of Internal Accounting. Internal accounting starts with the cost elements, which must be:

|

allocated to the different departments as indirect cost; | |

|

allocated to the different production cost accounts as direct cost; and | |

|

allocated to the different cost of goods sold as production cost. |