Costs of Goods Sold

Analysis Made for the Internal Accounting Configuration

By Emanuel Schwarz

(November 22, 1999) - We are now near the end of the basic discussion about the Internal Accounting. Throughout my series of articles, I have demonstrated the new idea of having a Chart of Accounts exclusively structured for internal transactions.

![]()

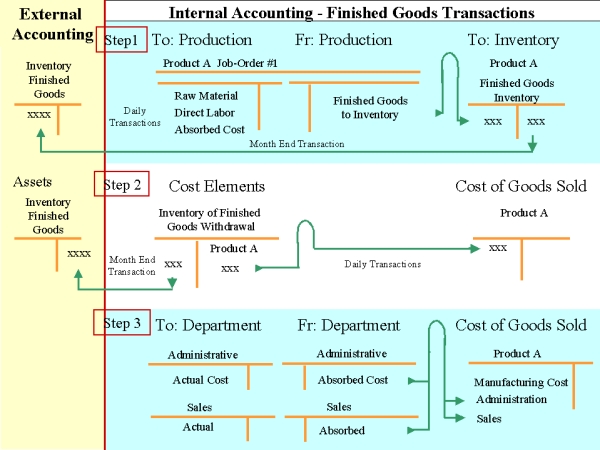

The graphics I have used offer a basic idea of the new Internal Accounting configuration.

Remember that the basic structure was established by the Class of Accounts. The Internal Accounting started with the identification of the different Cost Elements presented in Class 2.

All Direct Cost are allocated to Class 5 - were the Functional Activity accounts are established.

All Indirect Cost are allocated to Class 3 - which is the class of accounts that lists our different departments that the company has.

The Classes of 4 and 6 are so called "Contra accounts" for the Class 3 and 4. To class 4 we will credit the corresponding values of absorption that should be charged to the different products realized and recorded in Class 5.

Class 6 will be credited with the amount of production transferred to the Inventory of Finished Goods. These Inventory accounts are recorded in Class 7.

Let us now analyze what we have for accounts in Class 7 - the Class that we call Cost of Goods Sold. I have to tell you that this is the only Class in our Internal Accounting that actually has two different basic groups of accounts.

In the very beginning of this Class 7, we may observe three Groups of accounts that actually correspond to the Cost of Goods Sold.

We have the following three Groups:

7-1-00-0000 Finished Products Sold - will all the necessary details of the products sold during this accounting period.

Here you will be able to see immediately the first account in the next Class 8 with the account number 8-1-00-000 - that correspond to Revenues for Finished Products sold. This is the corresponding account of Class 7-1-00-000. This is a clear demonstration of how the External and Internal Accounting will work together.

7-2-00-000 Semi-Finished Products Sold - with all necessary details. Here, register the cost of these semi-finished products sold.

7-3-00-000 Special Selling Cost - of some production that still can be identified as our normal production/sales activity.

This Exhibit gives us the best indications of how the value of the Finished Product will be credited to the corresponding account in Class 6 [identified as From: Production] and transferred to the Finished Goods Inventory account of this same Product A. If possible we should use the Standard Production Cost for this transaction.

To end of each month, we have to transfer this amount from credit of Class 7 to the debit of the Inventory of Finished Goods account in Class 0. - Class 0 corresponds to the Permanent accounts of the Assets.

Let me clarify this, only month-end transaction may be recorded partially in the Internal and partially in the External accounting. In our case, we credit Class 7 that belongs to the Internal and debit Class 0 (Assets) that concur to the External accounting.

As the Exhibit shows, this transaction is identified as First Step.

The Second Step shows the amount of the Sales that we take out of the Inventory of Finished Goods - as a withdrawal - and charge to the account that corresponds to the Cost of Goods Sold, Product A.

Third Step refers to the Internal Accounting's transfer of the Administrative and Sales Department's Operating Costs to the Cost of Goods Sold of Product A. This procedure is done, to follow the instructions given by the Activity Based Costing [ABC].

Now we have clearly established the Cost of Goods Sold of some distinct group of products sold - or we may identify the Cost of Goods Sold of a specific product within such group.

With the speed and capacity of our computers, we can clearly establish the production cost of an individual product. We would indicate in the Inventory of Finished Goods the Production Cost of this product with detailed information of how much corresponds to the Direct Cost of Raw material, Direct Cost of Labor and the cost of one or several Direct Production Departments operating costs.