Values from External to Internal Accounting

An Analysis Made for the Internal Accounting Structure

By: Emanuel Schwarz

February 8, 1999 (Pro2Net) Last year we analyzed our new internal accounting structure in its basic configuration. We have learned how important it is to keep all recordings in internal accounting separate from External Accounting. We have seen in various graphics how internal accounting would be developed and have learned how the internal chart of accounts would be structured.

![]()

This year let us now study several important transaction details that need to be recorded within our internal chart of accounts. The first analysis will now refer to the question:

How will we transfer external expenditure values to our internal accounting structure?

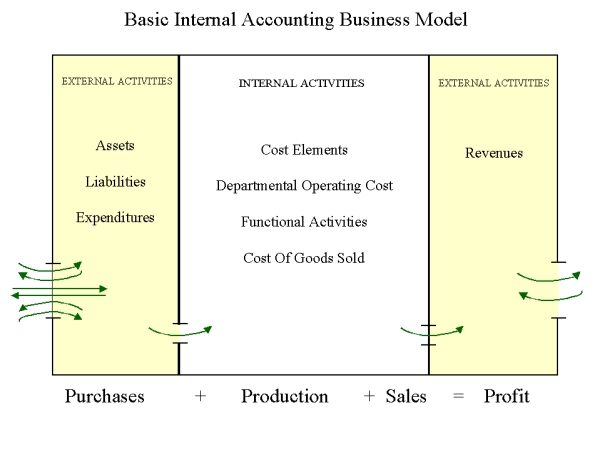

To understand this question better, let us look at the Graphic below. It shows us the basic picturesque configuration of external and internal accounting. To the left you will notice the area of external accounting that receives and registers all accounting data. From these recorded values we only need to transfer the expired portions into the internal accounting section. Here we will process these amounts as cost elements that are either directly or indirectly related with the different functional activities. We will accumulate specific amounts to establish the cost of production. Then we will take the cost of goods sold out to the external accounting section. This process is shown on the right side of the graphic.

Now that we have studied the basic presentation of external and internal accounting, let us analyze the important question of how to transfer the expenditure values debited in the external accounting section to the credit of the cost elements in the internal accounting section.

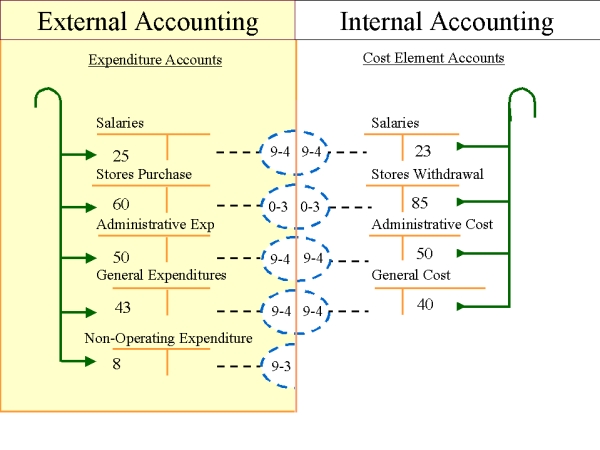

Graphic 01-02 represents the normal procedure to debit the different expenditure (expense) accounts with the corresponding amount of payment. Here we should record all those expenditure accounts that register outflow of payments. This means that we should also register the purchase of merchandise, spare parts, raw material, and fixed assets within this classification of accounts. At the end of each month, these amounts will be transferred to the corresponding accounts within Assets.

The right-hand side of this graphic shows the accounts with which internal accounting starts. This class of accounts is known as Cost Elements. All amounts that correspond to this accounting period's activities should be registered here. These amounts agree with the matching principals.

This means that we should also register the purchase of merchandise, spare parts, raw material, and fixed assets within this classification of accounts. At the end of each month, these amounts will be transferred to the corresponding accounts within Assets.

The right-hand side of this graphic shows the accounts with which internal accounting starts. This class of accounts is known as Cost Elements. All amounts that correspond to this accounting period's activities should be registered here. These amounts agree with the matching principals.

This graphic shows only four groups of accounts. As you can imagine, you could have up to nine groups, each with up to 99 main accounts 999 sub accounts. Once we have established these accounts, each day or week we will have to analyze the amount that was registered in the corresponding external accounting account.

In reality we will NOT simply copy these expenditure amounts, however we have to analyze each account and establish clearly if its total value should be taken to the internal accounting side, or if some type of adjustments must be done.

This is a sort of "fine tuning" that we must exercise from the very beginning of the development of internal accounting. We must scrutinize the expenditure account and address the following questions regarding how to record these expenditure amounts.

- Is this an amount that will be repeated each month?

- Should we record the exact amount that will be recorded in external accounting, or should we record a pre-established monthly amount?

- Are there amounts that will be recorded only in the Internal Accounting?

Detailed Analysis

The incorporation of the above-mentioned guidelines allows us to interpret in

detail how to best record the amounts in external accounting.

1. Monthly, fixed costs such as rent, lease, depreciation, etc., will be fixed in internal accounting, without the need to identify them in the expenditure class of accounts.

2. In external accounting we must record the exact amount of invoices that we receive each month. These specific amounts should include both dollars and cents. This is unnecessary in internal accounting. Instead we may establish a specific dollar amount as a monthly cost element (i.e., regular phone bills). We may use a monthly average amount, or a number rounded off to only dollars and not cents.

3. In the modern accounting structure of internal accounting, we may include cost elements that refer to the financing of projects with our company's own capital. Currently we are not permitted to include this cost of capital within external accounting expenses and production cost. We may also include specific cost elements that refer to research projects that we would record as functional activity.

I should also mention that external accounting uses non-operating expenditures. These expenditures refer to payments that have nothing to do with our specific functional activities. In other words, they have nothing to do with our business.

Month-end closing transactions

As Graphic 01-02 shows, each account in external and internal accounting is

identified with specific code represented by dotted lines. Expenditures are

debited with the actual amounts, then the dotted line moves from the credit side

of our expenditure accounts to an account identified with the code number 9-4.

This represents the transactions realized for closing entries. We must close all

expenditures by crediting their balance and transferring them to the account of

Class 9 and Group 4. This account belongs to the month-end-closing group.

Conclusion

Analysis of our expenditure accounts allows us to establish the corresponding

cost element values for internal accounting. We can now actually begin internal

accounting procedures, which we will discuss in our next month's article.