By Emanuel Schwarz

June 22, 1998 (Pro2Net) As we move toward a new millennium, many good people have been talking about the important changes in our activities the year 2000 will require. Should not we, accounting professionals, also revise our old-fashioned accounting structure and moved ahead toward the development of a more specific, internal accounting structure?

![]()

Our present accounting structure was developed some 80 years ago: At that time, no one was interested in internal accounting. Instead external accounting was developed, specifically for financial accounting purposes.

How is it possible, that during these many years, none of our top ten professors developed a structure specific to internal accounting, one that would serve managers in our industries to understand the economic development of their companies?

The answer may be found on page 14 of "Relevance Lost," by Thomas Johnson and Professor Robert S. Kaplan:

"One might wonder why university researchers failed to note the growing obsolescence of organizations' management accounting systems and did not play a more active or more stimulative role to improve the art of management accounting systems design. We believe the academics were led astray by a simplified model of firms' behavior."

These professors did not show any interest in studying the new approaches that exist in other countries. Even if they did accept these new internal accounting structures, it would be a very costly adoption, as it would require them to rewrite their present books. Likewise, auditing firms would have to reeducate their staff, which would also be a major financial investment. So thus far, we have used a rather old-fashioned chart of accounts.

However a new chart of accounts for internal accounting - one that will separate external accounting from internal accounting - could be implemented. This new structure would include:

| Cost elements that correspond to a specific accounting period | |

| Control of the responsibility accounting system | |

| Control of the reallocated indirect cost | |

| Control of the absorption cost system | |

| A functional activity cost system |

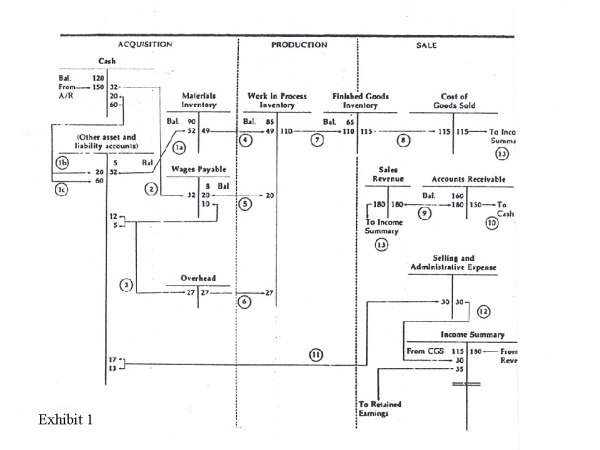

In Professor Emeritus Robert N. Anthony's book called, "Fundamentals of Management Accounting," observe how Anthony divides his flowchart into three basic structures (see the figure below):

Acquisition

Assets, liabilities and expense accounts are identified with the rather

inaccurate terminology of "overhead."

Production

Items here are identified in only one of two ways: the work in process inventory

(another inaccurate term) and the finished goods inventory.

Sale

Activities here are a mix of temporary and permanent accounts.

Although these structures have some flaws, Professor Anthony has given us this first glance of an external and internal part of our flowchart.

Students frequently ask me:

"Where are the expense accounts that we learned about in General

Accounting?

"Where are they represented in our Cost Accounting books?"

Since we have only one flowchart - for general accounting (specifically for financial accounting) we cannot have both expense and overhead accounts. Why? Because our overhead accounts (which represent the indirect costs we charge as departmental operating cost accounts) use the expenses of the month. As a consequence we cannot have both expense and overhead accounts.

Robert Kaplan addressed this problem in his book, "Advanced Management Accounting."

"With a greater realization of these internal uses of cost accounting data, accountants began devising cost accounting procedures that would be most relevant to a particular decision. Emphasis shifted from external to internal uses of cost accounting data. One could now think of recording cost data for internal purposes in a manner different from that used for external purposes."

Kaplan has also written several articles on the need for a separate cost system for internal use.

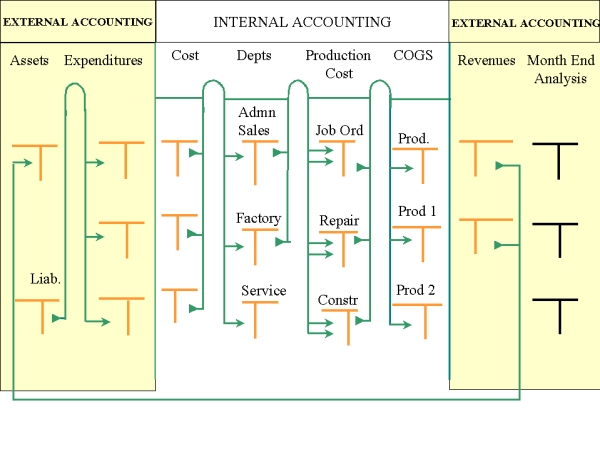

So let us develop a structure that works for internal accounting - one with a similar three-part structure that was previously outlined (see the figure below):

Acquisition

This refers to assets, liabilities, capital and expenditures.

Sale

This refers only to the sales activities and the accounts that show the results

of a given period.

Production

This section is specially developed for internal accounting, including:

| Class of accounts for the cost elements | |

| Class of accounts for the responsibility accounting system (departments) | |

| Class of accounts for the absorption costing and the reallocation | |

| Class of accounts for functional activity cost (production cost) | |

| Class of accounts for cost of goods sold |

Terms such as "overhead" are gone, replaced with terms that clearly identify the purpose of each account (i.e., departmental operating cost + the name of the specific department). The term "work in process" would also be replaced with the correct denomination of production cost accounts.

Students that have correctly understood the meaning of the term "work in process" - are generally astonished to learn that this term corresponds to the production cost of the month.