By: Emanuel Schwarz

January 11, 1999 (Pro2Net) Most professionals who have helped companies develop their production cost accounts know how difficult it is to work with an old fashioned structure such as the Work in Process account system.

![]()

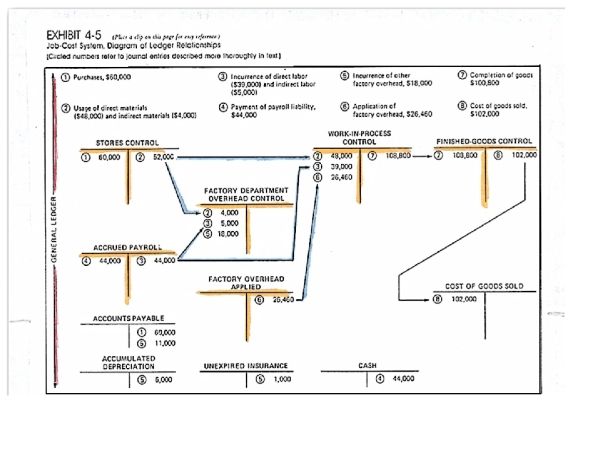

You may remember the Exhibit 5-4 in the Cost Accounting book prepared by Professor Charles Horngren of Stanford University. This exhibit was prepared 30 years ago and is still used today. It is unfortunate many professors are resistant to the modification of their exhibits and text into a more modern presentation.

Students have the impression that production companies need only one Work in Process account. As a consequence, that is just what in real life our companies have. Due to the high cost of re-training their employees, auditing companies support this one Work in Process account idea, and may not be prepared to open more accounts within Functional Activities accounts.

Here you see the following Exhibit, a presentation used by Professor Horngren:

For reference, look at the Illustration 3-8 prepared by Prof. E.B. Deakin in his Cost Accounting book. There is some confusion about the Manufacturing Overhead account and the Work in Process Inventory Assembly accounts. There is not an account that would refer to the product assembled and finished.

I would like to show you the new accounting structure under the description of Functional Activities that the advanced Internal Accounting developed. The functional activities of this Class 5 refer to the production costs of our products and also to the activities that we have in the company regarding maintenance and repair, and also to the construction and different projects that we may have in our company.

As you can see, under the title of Finished Products we have accounts to each and every product that we elaborate. And once the units are finished, they are accounting-wise transferred from credit Class 6 to debit of accounts in Class 7. These accounts in Class 7 have contra accounts to our Inventory accounts in the assets.

In same way, we have to control the Semi-Finished Products production. These are units that we produce, but we do not sell them, because it is not a finished product.

These accounts are not called Works in Process. It would be meaningless, to call an account as work in process. It is unfortunate that we have a name for our production cost account. Now with our Internal Structure we are not more compelled to use this incorrect terminology.

What is also important, is that we have created two specific classes of accounts: one for the amounts that we debit our production accounts - Class 5 "To the Functional Activities" - and the other for the values that we credit these production accounts - Class 6.

This new and very advanced structure makes it possible to avoid to mix same account values that we charge to the production and those that we transfer to the inventory of finished or semi-finished products.

The code structure is also clearly identified with the Class 5 as the first digit, next is the Group digit one, and followed by the two digits for the Main account.

As in this new structure we are using the terminology of the Functional Activities realized by our company. We consequently do not only refer to the production process but also to other important activities.

One of the next important activities that we have to control and give correct information to management, is the Preventive Maintenance. Preventive maintenance is extremely important, especially for companies with electronic equipment or other expensive units. Unfortunately, cost accounting books do not mention about maintenance. The present Chart of Accounts only refers to the external accounting; it is impossible to include control accounts for maintenance.

Now with the new Chart of Accounts referring also to the Internal Accounting, this important control of maintenance can be done without any complications. We may open specific accounts for the different maintenance activities. At the end of each month we will have to re-allocate specific maintenance costs to the corresponding direct production departments or directly to the corresponding production cost accounts. This is a specific decision that each company must make. Maintenance accounts will be opened for specific machines, for maintenance of trucks and buildings, etc.

The next control step will be to open accounts for the repair activities.

It is not always easy to identify maintenance from repair, but either way, some specific repair accounts will have to be created. During the month we will charge the repair costs to these accounts: some costs could be identified as direct, and the indirect costs will be absorbed from the repair departments operating costs. At the end of each repair, the total cost will be credited Class 6 and transferred to a corresponding account in Class 7.

As a last identification of the different Functional Activities, we must open accounts for the internal projects that our company may have. These internal activities refer to our company's production of specific tools for company's own use. Maybe our company is also building special machines or we may open accounts that will control research activities. In other words, these accounts are referring to special activities that Internal Accounting will have to control.