Why Work in Process (WIP) is Incorrectly Utilized.

Developing a "Chart of Accounts" for internal accounting.

By Emanuel Schwarz

Sept. 21, 1998 (Pro2Net) As described in my last two articles, "Benefits of Developing an Internal Accounting Structure," and "Why You Need an Internal Accounting Structure," - private accountants need to develop a completely new "Chart of Accounts" strictly for internal accounting. This Chart of Accounts should be structured specifically to fulfill the necessary information for management regarding internal development of their company.

![]()

My first two articles contained graphics that indicate the best way to develop the Internal Chart of Accounts is to completely separate these internal accounts from the transactions related to financial accounting (general accounting).

For example: in financial accounting, we credit accounts payable - and debit some expense. In the new Chart of Accounts - the term "expenditure" is recommended instead. Important to recognize is that in internal accounting, the term "cost" should be used - instead of "expense." The amount of this payment will show management how much the cash outflow was during this month. This approach should be expressed in Class 1 accounts.

As soon as expenditure is recorded, ask the question: "Should I correspond this expenditure also as a cost for this particular month of internal activity - directly or indirectly related with our administration, production or sales?"

If the answer is "yes," then credit the corresponding amount to a cost account. This cost account will be of the same type as the expenditure account.

As the internal accounting is developed, and a Chart of Accounts is independent of financial accounting, it is not necessary to establish terms that are absolutely wrong for the internal accounting, but needed in the financial accounting.

For example, consider the crazy denomination of the production cost account as a Work in Process account.

Every student who dedicated attention to the production cost account will know that the work in process amount corresponds to the difference between debit and credit amounts of such production cost account.

So the famous term WIP - is wrong terminology when talking about the production cost. But our dear professors and accountants - and all those good guys of the GAAP - had no other choice than to use this term of Work in Process as they did not have a separate Chart of Accounts for internal accounting.

And this incorrect terminology was established then subsequently supported for the last 50 years or more. As this production cost account had to be recorded in the assets of the company, there was no other choice than to name this account as WIP. But now, with the development of an internal Chart of Accounts - there is a perfect solution to this old dilemma:

The creation of a special "class of accounts" called - Production Cost Accounts. In the new production cost accounts, the class of accounts that is distinguished with the number 5 - is exclusively used to identify the production cost of the specific job order and related to this particular month.

These production cost accounts show the cost that have been charged to these accounts during the present accounting period. From Class 6 (the next group of accounts that is credited) the production cost of the job order is transferred to the inventory account - either semi-finished or finished products. This production cost can be transferred to a next step of the production process. That will be from credit Class 6 to debit Class 5 - where we will have to add new production cost.

The following graphic gives a picture of how the production cost accounts are processed.

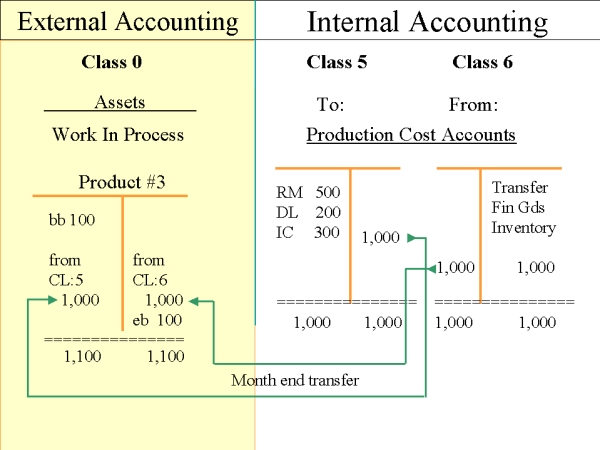

| To Class 5 production cost accounts we debit the different direct and indirect cost. During the month, some amounts are transferred every week (just as an example) to the finished goods inventory account. This is recorded from Class 6 to Class 7. At the end of the month, close these accounts by crediting Class 5 accounts with the same amount in the debit. | |

| This is the same way Class 6 accounts are closed. These closing values are then transferred to an asset account called Work in Process. This term is used here in an appropriate way because it shows just the work in process amount. | |

| This asset account will have a beginning balance, which corresponds to the amount of work in process from last period. No value of the work in process is debited in the internal accounting. | |

| As mentioned earlier, under Class 5 there are accounts corresponding to the values invested during the month for semi-finished and finished products. We can open under Class 5 accounts to show management the cost of maintenance and repair and the cost of producing some tools and machines for our own use. This approach is something absolutely new for cost accounting teaching. |

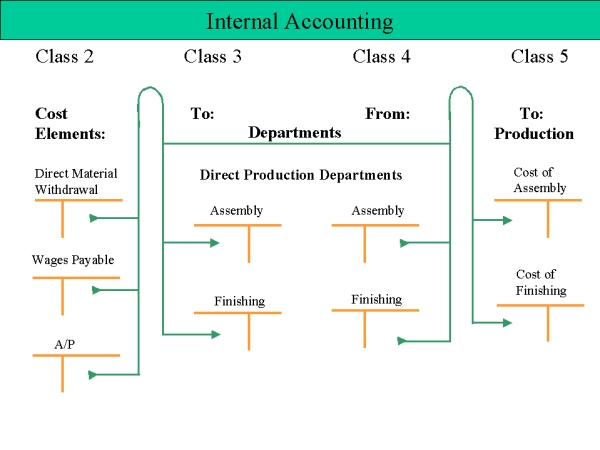

Consider Exhibit 1-9, Illustration of Flow of Costs:

This shows in detail how direct and indirect production cost is transferred - starting from Class 2: cost elements. These cost elements need to be credited and the debit charged to the direct production departments (there are two of them here) with all indirect cost. The direct cost is taken from credit cost elements and transferred to debit of the production cost accounts in Class 5.